Palantir’s Blowout Quarter: Growth + Profits at Scale

A concise, mobile‑first snapshot of the key numbers, context, and risks from Palantir’s third quarter 2025 results.

Key Performance Indicators

At‑a‑glanceQuick Summary

What mattersMini‑Charts

Visual pulseDeal Activity Snapshot

Scale & mix| Deal Size | Count (Q3’25) | Comment |

|---|---|---|

| ≥ $10M | 53 | Large‑scale enterprise commitments |

| ≥ $5M | 91 | Mid‑to‑large expansions |

| ≥ $1M | 204 | Broadening commercial footprint |

Market Context

What’s priced in?High expectations and valuation sensitivity can trigger profit‑taking. Investors debate sustainability of triple‑digit growth as base scales.

Bull vs Bear — What to Watch Next

Forward lens- Commercial flywheel keeps spinning (new logos + expansions).

- Margins stay healthy even as investment rises.

- Platform differentiation vs cloud & point tools persists.

- Analyst skepticism fades; institutional ownership deepens.

- Growth normalizes faster than expected on a larger base.

- Competitive pressure compresses pricing/margins.

- Regulatory or reputational shocks in sensitive sectors.

- Valuation de‑rates on macro or AI‑cycle cooling.

Notes & Method

Read meMetrics reflect publicly discussed Q3’25 highlights: ~63% Y/Y revenue growth; ~51% adjusted operating margin; Rule‑of‑40 ≈ 114; U.S. commercial Y/Y growth ≈ 121%; deal counts ≥ $1M/$5M/$10M: 204/91/53. Mini‑charts are illustrative (not to scale). This infographic is designed for fast mobile consumption with accessible colors, large tap‑targets, and no fixed headers.

Quick Snapshot

- Palantir crushed its Q3 2025 results: 63 % year-over-year revenue growth and a “Rule of 40” score of 114 %, according to Palantir’s own investor update. (Benzinga)

- U.S. commercial revenue alone grew 121 % Y/Y in Q3, to about US $397 million. (Palantir Investors)

- The company raised its guidance for Q4 and full-year 2025, showing strong confidence in its trajectory. (Investing.com)

- Yet, paradoxically, the stock dropped in pre-market trading following the results. The broader market appears wary, despite the strong numbers.

- In a high-volume interview snippet, CEO Alex Karp framed Palantir as a misunderstood company-and-movement, claiming the expert class got it wrong while the “average” investor got in and profited. (As an aside: Much of the quoted script aligns with Palantir’s known results and external reports.)

In this article we’ll unpack: the results themselves; what they signal for Palantir; what the cautious market reaction means; the rhetoric from management; and the major questions that remain.

1. The Results — What Really Happened?

Revenue growth & margin strength

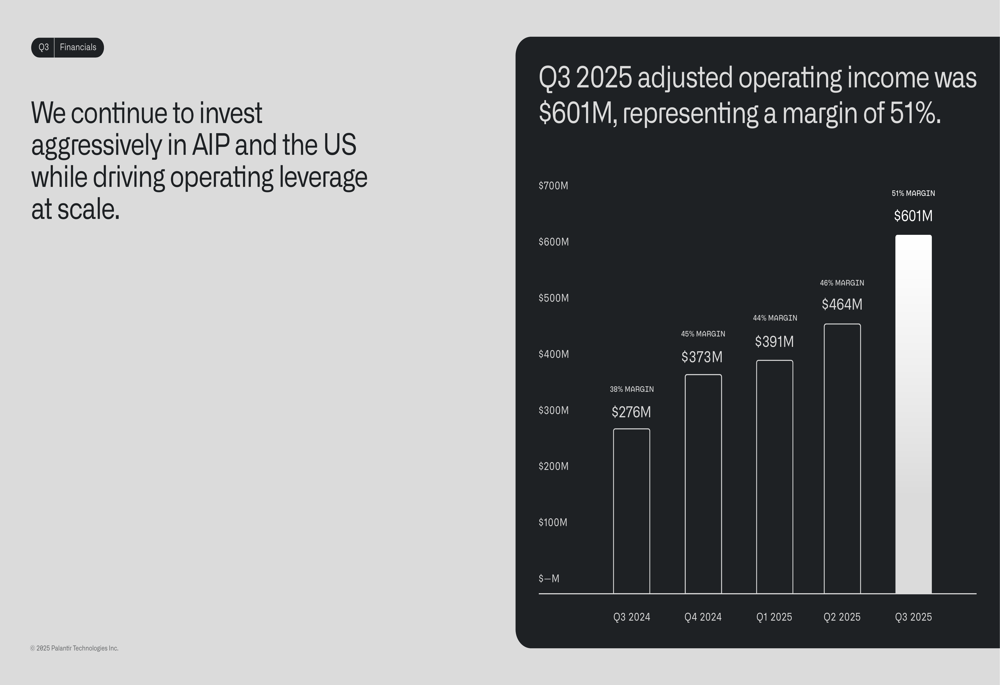

For Q3 2025, Palantir reported revenue growth of 63 % Y/Y to about US $1.18 billion. (Investing.com) Adjusted operating income came in at roughly US $601 million, corresponding to a ~51 % margin. (Palantir Investors) Combine those and you get what Palantir calls a “Rule of 40” score of 114 %: growth + margin well above the traditional benchmark of ~40 %. (Benzinga)

Commercial acceleration

The U.S. commercial business is a stand-out. Revenue grew 121 % Y/Y in that segment. (Palantir Investors) Q3 deal flow was strong: Palantir closed 204 deals of at least US $1 million, 91 deals of at least US $5 million, and 53 deals of at least US $10 million. (Palantir Investors)

Guidance raised

For Q4, Palantir is guiding revenue at ~US $1.327-$1.331 billion, and full-year 2025 at around US $4.396-4.400 billion. U.S. commercial revenue is expected to exceed US $1.433 billion, representing 100 %+ growth. (Investing.com)

Why these numbers matter

- A 63 % growth rate on a revenue base approaching (or above) US $1 billion is rare among large enterprise software firms.

- A 51 % margin at this stage indicates Palantir is scaling efficiently, not just burning cash.

- Achieving both strong growth and profitability is one of the key tests for a SaaS/AI‐software company — many companies grow fast but with weak margins, or have high margins but slow growth.

- The shift into U.S. commercial (beyond government contracting) suggests Palantir is broadening its addressable market, which is especially meaningful given its origin as a “government-defense” software company.

2. Why Is the Market Reacting With a Pullback?

Given the excellent numbers, why the down tick in pre-market / early trading? Several possible explanations:

Valuation expectations

When a company has already been richly valued, even stellar results can trigger profit-taking or skepticism about sustainability. Palantir has been discussed widely as a high-growth/AI play and that raises expectations. Indeed, analysts have cautioned that many AI-software names trade on future potential rather than current results. (Nasdaq)

Is the guidance baked in?

While Palantir raised guidance, sometimes the market discounts this because the guidance was already expected, or because the incremental step isn’t seen as large enough relative to the prior valuation and risk. The question then becomes: “What more can the company deliver going forward?”

Broader macro/sector risks

Technology and AI stocks can be volatile. Fears around regulation, slowing growth, or rising interest rates can dampen sentiment even when individual companies deliver. Some commentary on Palantir specifically note that despite its growth, valuation remains high relative to earnings. (Nasdaq)

** “Retail vs expert” narrative**

The script you provided touches on a divide: average investors vs “expert class” analysts/short-sellers. If the market perceives a disconnect between retail enthusiasm and institutional caution, that can create choppiness. Some short interest remains (albeit lower than prior levels) which can contribute to volatility. (Barchart.com)

In sum: great results, but the bar was high, and some questions linger about sustainability, valuation, and whether the “story” is fully priced in.

3. CEO Rhetoric & the Broader Narrative

The script you shared — in which Alex Karp states that Palantir is “anti-playbook,” that “average Americans got venture returns while the experts sit on the sideline,” and that short-sellers are constantly getting “screwed” by Palantir’s results — is emblematic of how Palantir frames its identity:

- A company that is unconventional (“we’re an anti playbook company”)

- A company that is misunderstood (by analysts, by “the expert class”)

- A company that positions itself as aligned with workers, with American competitiveness, with warfighters

- A company that emphasizes both value creation and moral/ideological purpose (“giving an unfair advantage to American workers, American war fighters and our investors”)

This kind of rhetoric serves several purposes:

- It builds a strong identity among retail investors and employees (us vs them)

- It reinforces the narrative of differentiation (not just “another software company”)

- It signals confidence (if you’re criticizing short-sellers, you’re implicitly asserting your strength)

- It implicitly addresses skepticism or criticism (“we are misunderstood”)

But there are also implications:

- When rhetoric is bold, execution must match. High claims raise expectations.

- The “us vs them” framing (retail vs analysts/shorts) can polarize sentiment: strong backing from one side, but entrenched skepticism from another.

- The narrative shifts focus from “just the business” to “the mission,” which may attract different investor types (those comfortable investing in purpose + performance).

For Palantir, this narrative aligns with the business: expanding from government defense into commercial AI/analytics gives it a unique positioning. The CEO’s comments about the “workers’ available GDP” and worker alignment in AI are interesting, in that they tie technology growth to broader economic/industrial themes.

4. So What Does This Imply for Palantir’s Future?

Given the results, guidance, and narrative, what should one watch? Here are key implications and fleshed-out questions:

Implication 1: Commercial growth is the lever

Palantir’s commercial business (especially U.S. commercial) is accelerating rapidly — 121 % growth Y/Y in Q3. If the company can sustain this expansion, the addressable market widens significantly.

- Question: Can Palantir maintain high-growth rates as the base gets larger? Growth percentages tend to moderate as companies scale.

- Question: Are the commercial wins repeatable, and do they have high margin/retention characteristics? High growth is great, but retention and expansion matter.

Implication 2: Margins and profitability are real factors

With a margin of ~51 % adjusted operating income, Palantir shows it’s not just growing fast but doing so profitably at this stage. That gives it more flexibility and credibility.

- Question: How much of this margin is sustainable, and how much is “optimistic” given scale/investment levers?

- Question: What level of investment in R&D, sales & marketing, infrastructure will be required to keep growth going, and how might that impact margins in future?

Implication 3: Valuation risk remains

When results are ahead of expectations, the stock may still pull back if valuation is high and growth expectations become even more demanding.

- Question: How much of Palantir’s growth is “priced in”? If investors expect 100 %+ growth for time to come, anything less may prompt a negative reaction.

- Question: Are there external risks (competitive, regulatory, macroeconomic) that could impair execution or margins?

Implication 4: Narrative & investor base matter

Palantir’s story is compelling to certain investor segments: those who like mission-driven tech aligned with defense/government/commercial AI, those who believe in retail investor momentum. But that also means the stock may respond more to sentiment than fundamentals.

- Question: Will institutional investors (who often drive large volumes) come around fully, or remain skeptical?

- Question: Will retail enthusiasm sustain, or does the stock risk being caught in a sentiment swing?

Implication 5: Short-sellers and market mechanics

The CEO’s comments about short sellers being “constantly getting screwed” reflect a real dynamic: high short interest can amplify volatility, both upside (short squeeze) and downside (negative sentiment reinforced). Indeed Palantir’s short interest has fallen but remains relevant. (Barchart.com)

- Question: To what extent is the stock movement driven by fundamentals vs trading dynamics (short interest, retail flows)?

- Question: If short interest is low, does that reduce potential upside from a short squeeze, or does it reduce a source of volatility?

5. Risks & Things to Monitor

Even with an excellent quarter, no company is without risks. For Palantir, some of the key risks and monitoring points include:

Competitive risk

As AI and analytics software become more important, competition intensifies from large cloud providers, other software vendors, and new startups. Palantir must continue to differentiate (platform, data, deployment, government relationships).

Customer concentration & switching

While Palantir is growing commercial business, it still has a meaningful government business component. Government contracting can be slower, but more stable — but it also carries political/regulatory risk. Ensuring commercial growth is sustainable and margins hold up will be key.

Execution risk at scale

Growth rates typically moderate as the revenue base grows larger. Going from $300 m to $600 m is much easier (percentage-wise) than going from $1.5 b to $3 b. Therefore, sustaining 100 %+ growth becomes harder. Palantir will need to keep expanding TAM, verticals, geographies.

Regulatory/social risk

Palantir is closely tied to defense, government intelligence/surveillance use cases, and there have been protests and controversy around both privacy and surveillance implications. (The Guardian) Reputation, regulation or public perception may affect which contracts Palantir can win or keep.

Valuation & sentiment risk

Because the company trades at a valuation premised on strong future growth, any sign of slower growth, weaker margin, or missing guidance may lead to sharp downside. Investors should monitor not just growth but also retention, deal size pipeline, margin trends.

Dependency on macro/AI cycle

Given Palantir’s positioning in AI and enterprise software, a broad slowdown in tech, tightening of enterprise budgets, or a shift in AI hype may impact growth. While Palantir appears ahead of the pack now, the broader environment matters.

6. Final Thoughts: Why This Quarter Matters

This quarter matters for Palantir for several reasons:

- It elevates Palantir from “promising AI/analytics player” to “high-performing, high-growth, high-margin software company” in the eyes of many. A 114 % Rule of 40 score is extraordinary.

- It opens the door for a re-rating (or at least serious reconsideration) by skeptics and analysts who may have dismissed Palantir as a hype play or niche government vendor.

- It strengthens Palantir’s narrative: commercial business taking off, defense/government business stable, margins strong, guidance raised — all of which support the meta-story of “software company scaling big, now.”

- However, despite the strong performance, the market’s cautious reaction highlights that execution going forward will be key — not just one quarter. Momentum must continue, the story must hold up, and the valuation must be justified.

For investors, the takeaway is: Palantir remains one of the more compelling high-growth software/AI plays, but it carries the risk baggage of any stock trading at a premium valuation. The big questions now are: can Palantir deliver at scale, can it keep expanding its commercial business at similar rates, and can it avoid pitfalls (competition, regulation, dilution, customer attrition)?

From a broader perspective, Palantir’s performance also speaks to one of the major themes of the time: enterprise AI, software that delivers quantifiable business value (not just hype), commercial adoption of data/AI systems, and defense/commercial convergence in tech. Palantir is positioning itself as a leader in all of those.

7. Summary Table

| Metric | Q3 2025 Highlights | Implication |

|---|---|---|

| Revenue growth (Y/Y) | ~63 % to ~$1.18 billion (Investing.com) | Strong top-line momentum |

| Adjusted operating margin | ~51 % (Palantir Investors) | Scalable business model, profitability matters |

| “Rule of 40” score | ~114 % (Benzinga) | Exceptionally strong by SaaS/enterprise standards |

| U.S. commercial revenue growth | ~121 % Y/Y to ~$397 million (Palantir Investors) | Commercial business gaining traction rapidly |

| Guidance raised for Q4 & FY2025 | Revenue ~$1.327‐1.331 billion in Q4; FY revenue ~$4.396-4.400 billion (Investing.com) | Confidence in forward trajectory |

| Market reaction | Pre-market shares down despite results | Valuation/expectation gap remains |

8. What I’d Recommend Watching in the Next Quarter

If I were tracking Palantir, here are the “watchpoints” I’d focus on:

- Commercial customer additions & deal size: Are the deals bigger, more frequent? How many new customers vs expansion within existing customers?

- Customer retention/renewal: Does Palantir keep customers long-term, or is there churn? Growth is good, but retention ensures sustainability.

- Margin trends: Are margins stable, improving, or under pressure from investment? Does the company need to invest heavily (which might compress margins) to continue growth?

- Guidance for Q1/2026 (if given): What are the assumptions for next year? Does management raise, hold, or lower expectations?

- Competitive wins/losses & vertical expansion: Which industries/geographies is Palantir winning in? Are there emerging verticals (energy, manufacturing, automotive, etc.) where Palantir is gaining ground?

- Narrative vs consensus shift: Are analysts upgrading? Is sentiment changing? Are institutional investors increasing their holdings?

- Macro/AI ecosystem shifts: For example, do enterprise budgets shift? Are there regulatory changes in AI/data/privacy that could slow Palantir’s growth?

9. Conclusion

In short: Palantir’s Q3 2025 results are very strong — rare in the enterprise software world. The company is growing quickly, generating healthy margins, and executing in a major way. From a business standpoint, this quarter validates many of the claims Palantir has made about scaling, commercial transition, and AI-software leadership.

Yet, the “tweak” in market reaction reminds us: in a market of high expectations, even great results must deliver more than what’s already anticipated. The valuation remains rich, and the broad environment remains uncertain (macro, AI hype, competition, regulation).

For long-term believers in Palantir’s mission and execution, this quarter may represent a meaningful inflection point. For cautious investors, the key is: sustainability of this growth and margin story. If Palantir can deliver similar or better results in subsequent quarters, the narrative may shift from “very promising” to “dominant software company.”

But if there is a hiccup — even small — the valuation premium means downside risk grows.

In that context, Alex Karp’s rhetoric (about being misunderstood, about short-sellers, about the divide between average investors and experts) makes more sense: this is not just a financial story for Palantir, it’s a mission story, a narrative story, and a technology story. The question for investors is: does the mission align with the execution, and will the execution continue to outpace the mission’s lofty claims?

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Always do your own research or consult with a financial advisor before making investment decisions.